How Decision Analysis Can Inform the Psychology of Regret

I recently wrote a memorial in honor of Dr. Ron Howard who taught me how to live a no regrets life. So when psychology professor Catherine Sanderson, PhD recently posted an article titled “The Best Strategy for Avoiding Regret? Take a Chance: Why Regrets of Inaction Haunt Us the Most“, I clicked right away and read the post twice. After reading Sanderson’s post one more time, I believe I have processed how to incorporate the psychology of regret into the decision analysis framework that relieves decision-makers from feeling regret. In essence, the value from learning from bad outcomes is a key wildcard in swinging a decision-maker between taking action and settling on inaction. Decision-makers are more likely to take action when the learning from bad outcomes is both actionable and valuable. The learning reduces the cost of bad outcomes and helps improve the odds of future good outcomes.

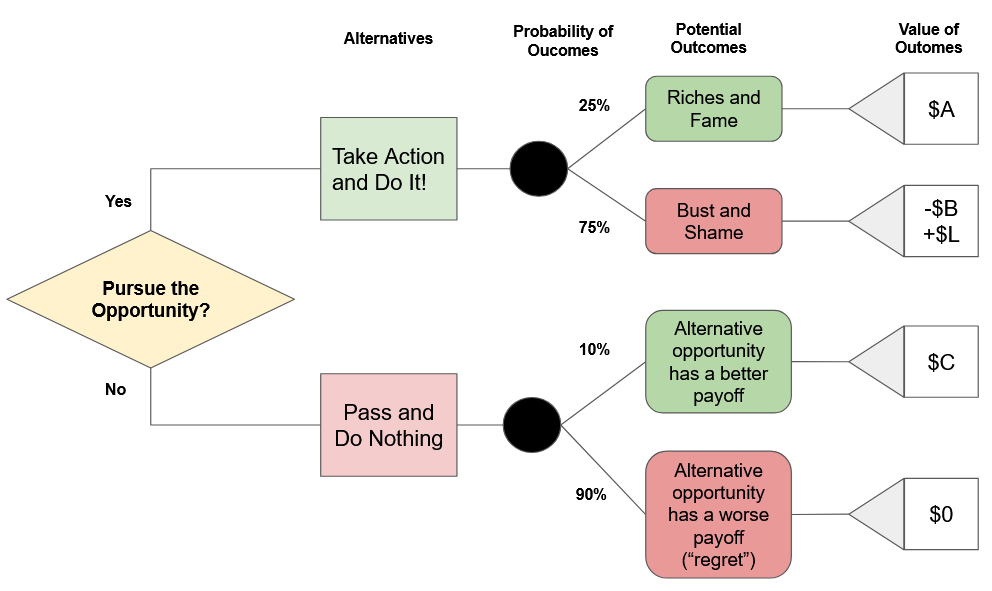

There are multiple ways to frame this problem. I chose the following simplistic (and stylized) decision tree for the purposes of this discussion:

From left to right, the following list describes this decision tree:

- The Decision: Answer the question “Pursue the Opportunity?” and follow through on that answer.

- The Choices: There are two choices (binary).

- Answering the question with a “yes” means “take action and do it”, pursue the opportunity.

- Answering the question with a “no” means “pass and do nothing”, do not pursue the opportunity.

- Potential Outcomes from taking action.

- A 25% chance of achieving “riches and fame” with a large payoff valued at $A (dollars)

- A 75% chance of suffering “bust and shame” with a cost of $B. Along with the failure comes learning valued at $L which can be applied to make better decisions going forward.

- Potential Outcomes from doing nothing.

- A 10% chance that the “alternative opportunity” has a better payoff than taking action now. Presumably, a future opportunity that appears better than the first opportunity dissolves nagging thoughts of regret. (This part of the framework could be expanded into another set of decision trees).

- A 90% chance that the alternative opportunity has a lower payoff and produces the kind of regret that Sanderson describes. For the purposes of this exercise, this outcome gets a zero value to represent a strong desire to avoid regret. This regret comes when the decision-maker looks back and wonders how life could have been better if only they had take the first opportunity.

According to Sanderson, “we experience more regret over things we choose not to do than things we choose to do.” We should choose action over inaction because the emotional response from the regret of taking action can be tangibly addressed by learning and increased knowledge. In other words, we can find the value in the action no matter the outcome. Regrets from inaction can leave lingering unanswered questions about what could have been. Inaction does not produce (direct) learning. Instead, inaction fosters the kind of doubt that entrenches regret.

The decision analysis framework provides a method for assessing whether the learning from a bad outcome can “push” the decision-maker toward taking action. Note well that I have purposely avoided describing a bad outcome as a mistake. A mistake in this context is only known after the fact and is uncontrollable after a (well-informed) decision gets implemented. Interestingly enough then, this framework also removes the regret from inaction. The no regret life starts with fully informed decisions (like decisions made using the decision chain). Thus, taking the time to fully assess the opportunities, alternatives, risks, costs, and benefits preserves the path of a no regrets life even when we choose to pass on an opportunity.

Assessing the No Regrets Decision-Making Framework

“Expected value” is the key concept for processing the decision-making framework. The expected value of a decision is the sum of at least two quantities. In this example, the expected value of taking action is the sum of multiplying the probability of the riches and fame (25%) times the value of the riches and fame ($A) plus multiplying the probability of experiencing the bust and shame (75%) times the value of the learning ($L) minus the cost of the bust and shame ($B). This expected value provides a simple way of quantifying a decision and comparing it to alternative decisions. In this case, the alternative decision is pass and do nothing (and create a path to an alternative opportunity).

The expected value also assumes the decision-maker is risk neutral. A risk neutral decision-maker neither seeks out risk nor avoids risk. For example, when faced with a 50% chance of winning $10 and a 50% chance losing $10, the risk neutral decision-maker is indifferent about taking the bet. They can “take it or leave it” given the expected value is $0 ((0.50 * $10) – (0.50 * $10)). A risk seeker will tend to take the bet because they are focused on winning the $10. The risk avoider will tend to decline the bet because they fear losing the $10. Finally, this definition assumes that the $10 is inconsequential to the bettor’s wealth.

The math for processing this framework is in the Appendix. Without the math, the decision-maker can use this framework to conceptually get explicit about the factors important to the decision. For example, the odds of bust and shame are very high. So the value of learning must be high and/or the cost be low to motivate taking action. Similarly, since the odds that an alternative will give a higher payoff (expected value) are relatively low at 10%, then the value of the alternative needs to be very high (in this case, 10 times the expected value of taking action!).

The upside from this decision analysis comes from bypassing feelings of regret from inaction. There is both value in the action of the doing and the value of discernment. While psychology advises a “bias” for action when potential benefits lie ahead, achieving clarity on the costs, the alternatives, and the value of learning can help the decision-maker. The decision-maker can more confidently pursue a no regrets life even if inaction becomes the chosen alternative.

The decision-making framework suggests that the bigger the potential cost of a bad outcome, the more learning needs to come from that potential outcome. Large potential benefits from a good outcome lower the necessary learning from a bad outcome to motivate the decision to act. Inaction is justified when the likelihood of an alternative yielding greater expected benefits is sufficiently high.

Questions? Need more clarity? Feel free to use the comment section below!

Follow Ahan Analytics, LLC on Facebook or LinkedIn and get notifications for the next analytic thoughts!

Appendix

The decision analysis framework allows the quantification of the decision. Since the ability to learn from bad outcomes is a major enabler of taking action, let’s use the framework to quantify just how much learning is required from a bad outcome to make taking action worthwhile.

The expected value of taking action is EVA = (pA) * A + (pB) * (-B + L) where pA is the probability or odds of outcome A, and pB is the probability of outcome B. pA + pB = 1

The expected value of taking no action is EVNA = (pC) * C + (pD) * 0 where pC is the probability of outcome C and pD is the probability of outcome D (with a zero value).

If EVA >= EVNA, then take action and do it! Equivalently, pA * A + pB * (-B + L) >= pC * C + pD * 0

Given pA + pB = 1, then solving for the required value of learning produces the following equation:

L >= (pC/pB) * C – (A/pB) + A +B

The value of learning (L) must be at LEAST as big as the components on the right-hand side of the equation to make the risk neutral decision-maker willing to take the opportunity now instead of moving on to take a chance on the alternative opportunity.

The simplest feature of this equation says that the bigger the cost (B) of the bad outcome (bust and shame), the bigger the learning must be to move forward with the first first opportunity.

The probability of the bad outcome, pB, has two effects. Firstly, as the probability of the bad outcome increases, the less positive is the impact generated by the good outcome. In the other direction, there is a point at which the probability of the bad outcome is small enough that learning can be zero and the decision-maker will remain motivated to take action. Secondly, as the probability of the bad outcome increases relative to the probability of an alternative achieving the better outcome (pC/pB), the value of learning must increase to motivate a decision-maker to take action.

Plug this formula into a program or spreadsheet and play around with a whole host of scenarios!